timbop

Well-Known Member

- First Name

- Tim

- Joined

- Jan 3, 2020

- Threads

- 65

- Messages

- 6,832

- Reaction score

- 14,036

- Location

- New Jersey

- Vehicles

- Solar powered 2021 MME ER RWD (CA RT1)

- Occupation

- Software Engineer

The mistake you are making is that the Ford options program is not actually a LEASE - you have 3 options at the end of the term:Actually I'm only focusing on the short term in the sense of doing options is a 3 year "lease" and so I was considering the alternative to that. Such as would it be better to run a 72 month financing and how would that compare in three years to the 36 month ford options. Actually in three years with 72 months financing and $15k down you actually pay more than the 36 month ford options, but I almost feel like it kind of balances out since I can only imagine the GT would be worth at least $30-35k at that point if not morend you'd effectively make back any potential loss on financing (just speculation since it's the top of the line model). Even 2017 Mustang GTs are selling right now in the high $20's.

This whole thing has been super confusing to figure out which is better but it may come down to just saying either one is just as good. The 72 month financing I feel like would have a good resale option in 3 years just in case I want to get out of the car at that point, but the 36 month ford options would have lower payments and a higher buy back if I wanted to keep it.

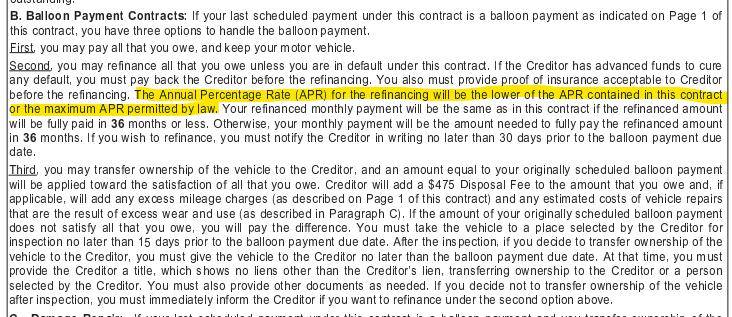

- return the car and walk away

- refinance/pay cash to buy the car out at the prescribed price

- roll any equity you have in the car over to another Ford vehicle (without having to buy it out first)

The real reason I did the options plan is in the event that solid state batteries are becoming available and the residual value of the Mach E drops significantly. In that case I would just walk away from the car and buy another BEV with a much better battery that has longer range and DCFC's much faster. If such a car isn't at least on the horizon, then I'll buy out my Mach E.

Sponsored