nhammerschmidt

Well-Known Member

- First Name

- Nick

- Joined

- Aug 30, 2021

- Threads

- 14

- Messages

- 168

- Reaction score

- 178

- Location

- 44272

- Vehicles

- 2021 VW ID.4

- Thread starter

- #1

I have a bit of a background in auto finance, so I wanted to walk through a potential purchase for everyone here using Ford Options.

I have a 2022 Mustang Mach-E Premium ER on order. The MSRP is $57,140, I live in Ohio and my tax rate is 7%

I have X-Plan and my dealer has agreed to sell it at X-plan.

X- Plan Price: $56,272.20

Doc Fee: $100.00

Sales Tax: $1,111.05 (Ohio taxes on the trade difference so I calculated the tax figuring an estimated trade value of $40,500)

License Fee: $35.00 (Transfer plates from current EV.) Ohio charges a $200 per year surcharge for Plug in vehicles.

Subtotal: $57,518.25

Rebates: -$2,750.00 (Ford Options on the calculator for my region shows $2000 in incentives and I have a $750 PCO resulting from the 2021 to 2022 conversion)

Deposit: -$500.00

Total: $54,268.25

For the sake of simplicity I am going to assume no money down. I drive a ton so I am figuring the options payment at 19,500 miles per year. Based on these parameters, the balloon amount is as follows:

36 months: 40% of MSRP ($22,856.00)

48 months: 33% of MSRP ($18,856.20)

At 2.49% APR (what is showing on the calculator for my region) here are the payments:

36 months: $953.89

48 months: $814.99

Ford offers mileage options at 7500, 10500, 12000, 13500, 15000, 16500, 18000, and 19500. Basically for every mileage band you go down from the 19,500 I put above you add 1% to the percentages I put above. So if you chose 36 months and 7500 miles, the balloon % would be 47%.

When a dealership does a Ford Options contract, there should be a spot in their dealer management system that says "balloon amount" The dealership would simply fill the appropriate balloon amount into that field and the payment should calculate for them and print correctly on their contract. In the payment disclosure section it would read something like this:

35 monthly payments of $953.89 beginning on 2/2/2022

1 payment of $22,856.00 due on 3/2/2025

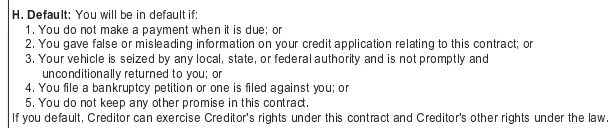

The paperwork is a standard FMCC installment contract there is no special contract for Ford Options. There is an additional addendum that the dealer has to submit that explains the options at the end of the 36 months:

Keep and pay the balloon in full

Refinance (in some states Ford is REQUIRED to refinance the contract on request from the customer)

Turn back into Ford (Subject to mileage overage, + excess wear and tear charges)

I hope this has been helpful for everyone. Please do not get caught up in the APR or rebates. Those vary by region and individual customer (if you have a private offer). Ford, in the past, has offered incentive protection on ordered units so that you got the better of the rebates at the time of order or at the time of delivery. Many of us ordered a 2021 and had them converted to a 2022. I am not sure that incentive protection works across model years, although I think it would be the right thing for Ford to do.

Let me know if you have any questions.

I have a 2022 Mustang Mach-E Premium ER on order. The MSRP is $57,140, I live in Ohio and my tax rate is 7%

I have X-Plan and my dealer has agreed to sell it at X-plan.

X- Plan Price: $56,272.20

Doc Fee: $100.00

Sales Tax: $1,111.05 (Ohio taxes on the trade difference so I calculated the tax figuring an estimated trade value of $40,500)

License Fee: $35.00 (Transfer plates from current EV.) Ohio charges a $200 per year surcharge for Plug in vehicles.

Subtotal: $57,518.25

Rebates: -$2,750.00 (Ford Options on the calculator for my region shows $2000 in incentives and I have a $750 PCO resulting from the 2021 to 2022 conversion)

Deposit: -$500.00

Total: $54,268.25

For the sake of simplicity I am going to assume no money down. I drive a ton so I am figuring the options payment at 19,500 miles per year. Based on these parameters, the balloon amount is as follows:

36 months: 40% of MSRP ($22,856.00)

48 months: 33% of MSRP ($18,856.20)

At 2.49% APR (what is showing on the calculator for my region) here are the payments:

36 months: $953.89

48 months: $814.99

Ford offers mileage options at 7500, 10500, 12000, 13500, 15000, 16500, 18000, and 19500. Basically for every mileage band you go down from the 19,500 I put above you add 1% to the percentages I put above. So if you chose 36 months and 7500 miles, the balloon % would be 47%.

When a dealership does a Ford Options contract, there should be a spot in their dealer management system that says "balloon amount" The dealership would simply fill the appropriate balloon amount into that field and the payment should calculate for them and print correctly on their contract. In the payment disclosure section it would read something like this:

35 monthly payments of $953.89 beginning on 2/2/2022

1 payment of $22,856.00 due on 3/2/2025

The paperwork is a standard FMCC installment contract there is no special contract for Ford Options. There is an additional addendum that the dealer has to submit that explains the options at the end of the 36 months:

Keep and pay the balloon in full

Refinance (in some states Ford is REQUIRED to refinance the contract on request from the customer)

Turn back into Ford (Subject to mileage overage, + excess wear and tear charges)

I hope this has been helpful for everyone. Please do not get caught up in the APR or rebates. Those vary by region and individual customer (if you have a private offer). Ford, in the past, has offered incentive protection on ordered units so that you got the better of the rebates at the time of order or at the time of delivery. Many of us ordered a 2021 and had them converted to a 2022. I am not sure that incentive protection works across model years, although I think it would be the right thing for Ford to do.

Let me know if you have any questions.

Sponsored

Last edited: