Motomax

Well-Known Member

- First Name

- Max

- Joined

- Jul 19, 2021

- Threads

- 5

- Messages

- 1,019

- Reaction score

- 1,027

- Location

- California

- Vehicles

- VW GLI, 4Runner

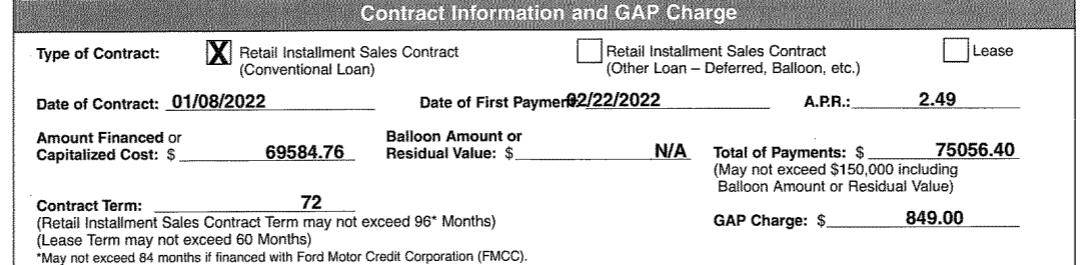

Are you sure there including the incentive because your contract says 0 under manufacturer rebates. Or is that your old contract. I didn’t quite follow your whole situation haha.Yup. They definitely bent me over. It's a good lesson to have. I'll learn from it.

I'm trying to get them to include the $750 clean fuel reward, but they are not familiar with that and are not listed as one of the "participating dealers" on the incentive's website. So not going to rely too much on that one. They're including the $2,500 incentive.

?

Sponsored