Anton

Well-Known Member

- First Name

- Anton

- Joined

- Jan 10, 2022

- Threads

- 15

- Messages

- 267

- Reaction score

- 213

- Location

- Fresno, CA

- Vehicles

- 2021 Mach-E AWD ER

- Thread starter

- #1

Hello there,

Some preface... What I'm trying to make sure here is that I don't get f***ked by the dealership/finance guys out of money. So I'm asking for advice on how I should handle this situation moving forward. Please help me get out of this mess...

At time of purchase of my Mach-E the guys said that Ford Options was not an option in California (wrong). I said lets go ahead with regular financing because I wanted to take the car home with me that day. After speaking with their GM about Ford Options, he said that they will re-do my contract. Effectively cancelling the current contract and starting a new one with Ford Options. I will be the first one at their dealership to get Ford Options. After briefly meeting with the finance guy today to look at some preliminary numbers, to my surprise the Ford Options monthly payment total came out to be exactly the same as my regular financing - ~$1,050/mo. Something smells fishy here...

Car sale price - $64,000 (includes $8,000 ADM)

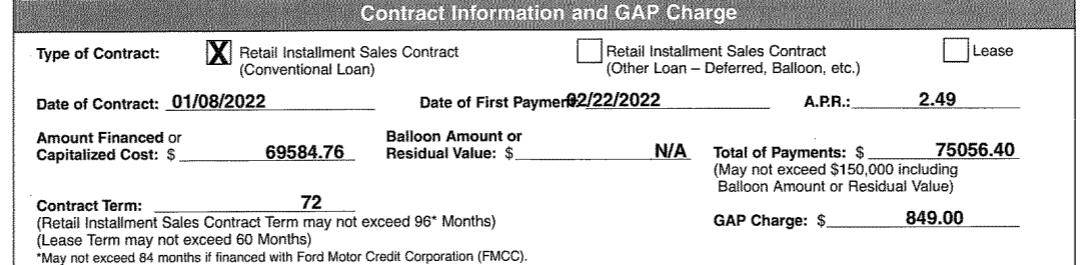

Regular finance purchase -72 months, 2.49%, $6,400 down.

Ford Options Plan - 48 months, 2.49%, 10,500 miles/yr, $6,400 down.

Credit score -~770.

Upon checking and comparing to the estimating payment on the Ford Build-a-Mach-E website I saw some MAJOR differences. Their estimate was that I should be paying roughly $680/mo with a sale price of $64,000 and $6,400 down (website did give me a estimated APR of 1.4%, but shouldn't be that big of a difference).

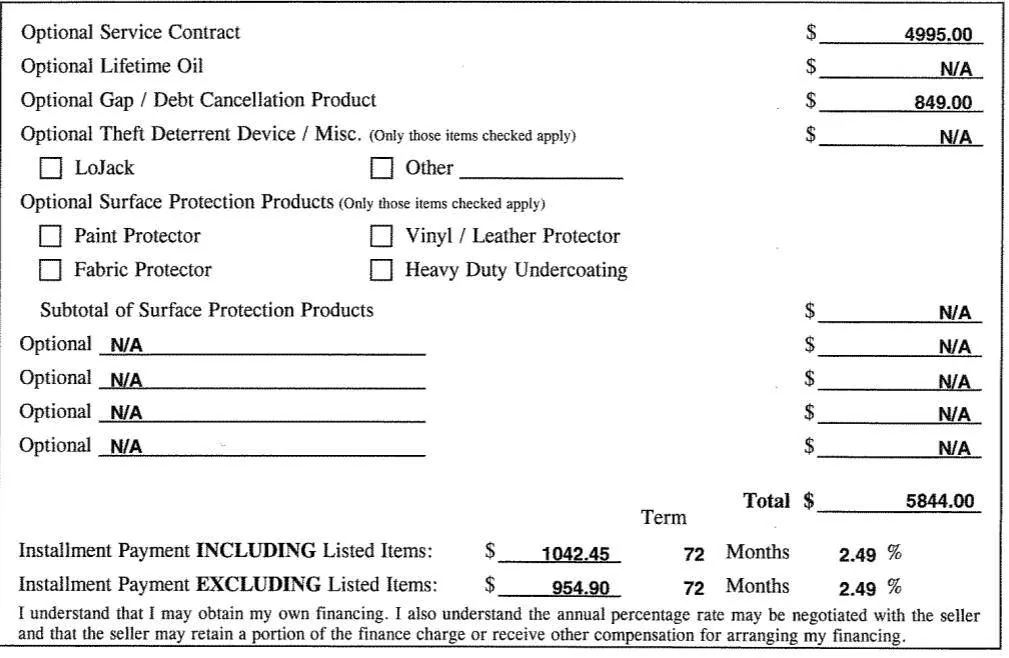

Now that I look back on the day of purchase there was a major red flag that I looked past. The finance guy said that I will only be able to get the 2.49% if I get the extended warranty and GAP protection. My original APR was like 3.49%. This would only raise my monthly bill by $10. "No brainer, right?" (His words). I said sure, let's add the extended warranty and GAP protection... There was also some fees involved during the process that I looked past (I will post my original contract details below).

What I think is happening now is that they are trying to get me to pay the same fees and buy the extended warranty + GAP protection with the Ford Options plan. Hence the big price difference... Since they are cancelling my original contract, can I avoid purchasing the extended warranty, gap, and argue for them to not include these absurd fees (e.g. $4,995 optional fee to the Ford Motor Service Company, I guess this is the extended warranty)?

Here's my original contract details (in process of getting nullified/cancelled in favor of a Ford Options contract):

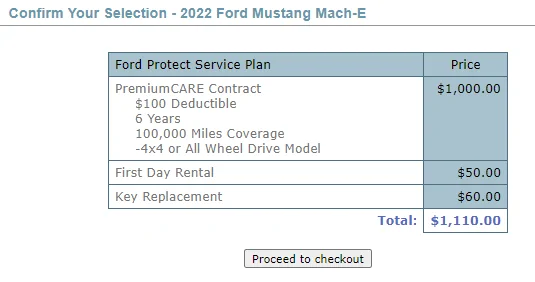

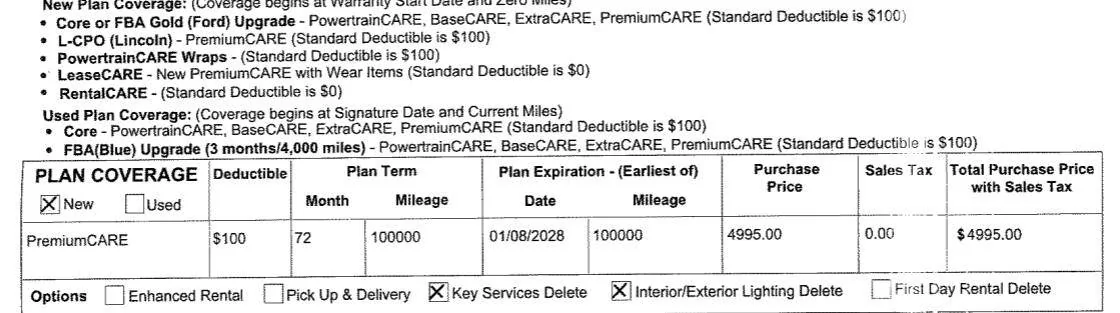

EXTENDED WARRANTY

GAP:

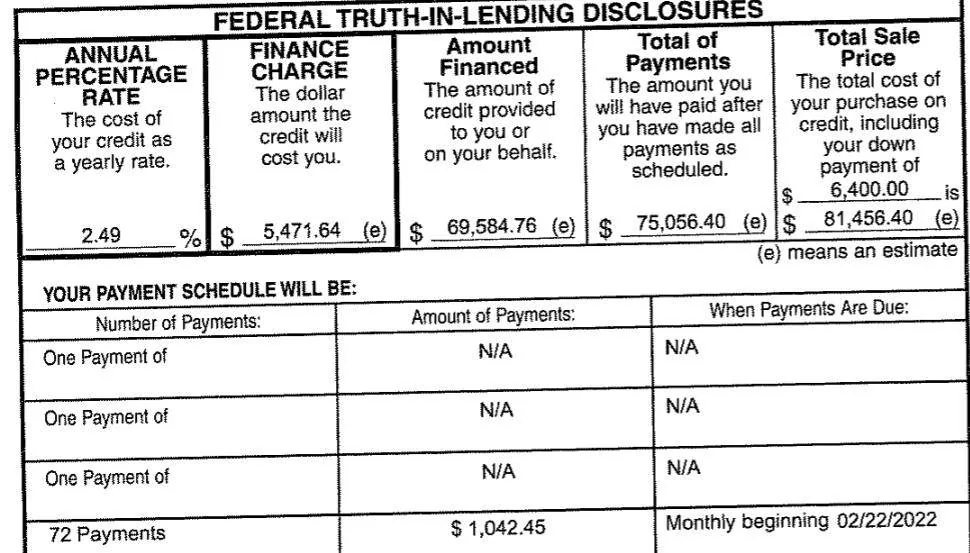

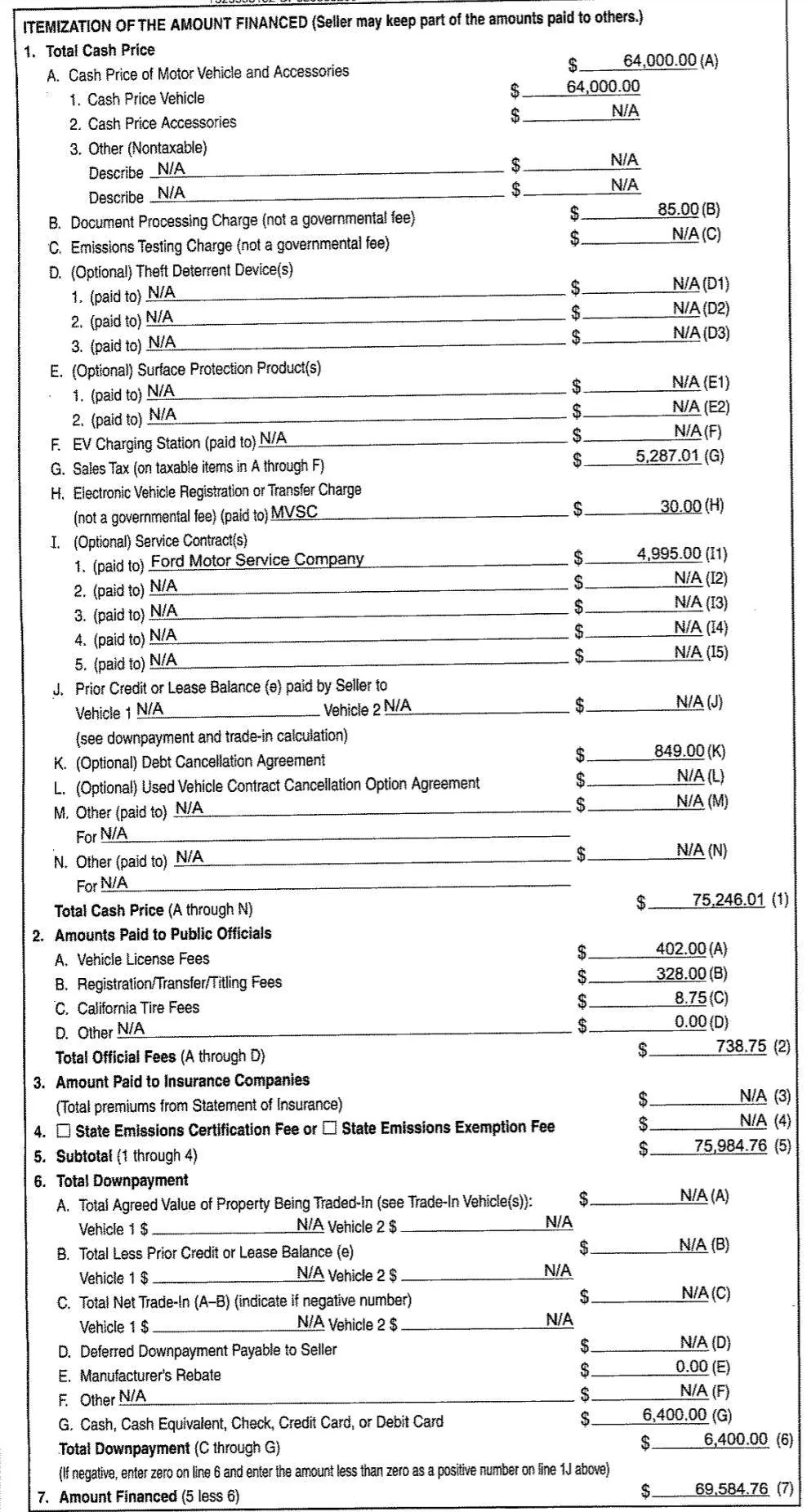

VEHICLE CLOSING STATEMENT:

In summary:

1. Can I reject the extended warranty and GAP protection from my original contract agreement which will be nullified prior to starting the Ford Options agreement? Dealership is trying to keep these...

2. Is it true that to get a lower APR I have to get extended warranty?

3. What APR should I be expected to pay with a ~770 credit score and 10% down?

4. I'll take any advice you can give me.

Some preface... What I'm trying to make sure here is that I don't get f***ked by the dealership/finance guys out of money. So I'm asking for advice on how I should handle this situation moving forward. Please help me get out of this mess...

At time of purchase of my Mach-E the guys said that Ford Options was not an option in California (wrong). I said lets go ahead with regular financing because I wanted to take the car home with me that day. After speaking with their GM about Ford Options, he said that they will re-do my contract. Effectively cancelling the current contract and starting a new one with Ford Options. I will be the first one at their dealership to get Ford Options. After briefly meeting with the finance guy today to look at some preliminary numbers, to my surprise the Ford Options monthly payment total came out to be exactly the same as my regular financing - ~$1,050/mo. Something smells fishy here...

Car sale price - $64,000 (includes $8,000 ADM)

Regular finance purchase -72 months, 2.49%, $6,400 down.

Ford Options Plan - 48 months, 2.49%, 10,500 miles/yr, $6,400 down.

Credit score -~770.

Upon checking and comparing to the estimating payment on the Ford Build-a-Mach-E website I saw some MAJOR differences. Their estimate was that I should be paying roughly $680/mo with a sale price of $64,000 and $6,400 down (website did give me a estimated APR of 1.4%, but shouldn't be that big of a difference).

Now that I look back on the day of purchase there was a major red flag that I looked past. The finance guy said that I will only be able to get the 2.49% if I get the extended warranty and GAP protection. My original APR was like 3.49%. This would only raise my monthly bill by $10. "No brainer, right?" (His words). I said sure, let's add the extended warranty and GAP protection... There was also some fees involved during the process that I looked past (I will post my original contract details below).

What I think is happening now is that they are trying to get me to pay the same fees and buy the extended warranty + GAP protection with the Ford Options plan. Hence the big price difference... Since they are cancelling my original contract, can I avoid purchasing the extended warranty, gap, and argue for them to not include these absurd fees (e.g. $4,995 optional fee to the Ford Motor Service Company, I guess this is the extended warranty)?

Here's my original contract details (in process of getting nullified/cancelled in favor of a Ford Options contract):

EXTENDED WARRANTY

GAP:

VEHICLE CLOSING STATEMENT:

In summary:

1. Can I reject the extended warranty and GAP protection from my original contract agreement which will be nullified prior to starting the Ford Options agreement? Dealership is trying to keep these...

2. Is it true that to get a lower APR I have to get extended warranty?

3. What APR should I be expected to pay with a ~770 credit score and 10% down?

4. I'll take any advice you can give me.

Sponsored

Last edited: