hybrid2bev

Well-Known Member

If you want to keep the vehicle past the monthly payment term then yes you would need to either refinance or pay off the final balloon payment amount.I had thought I read somewhere that you could also keep the car, after the 36 months and just keep paying the same payment for an additional 3 years or something. Is this not the case? So you have to refi if you want to keep the car and cannot just pay the lump sum balloon?

You'll want to read the language on your contract before signing.

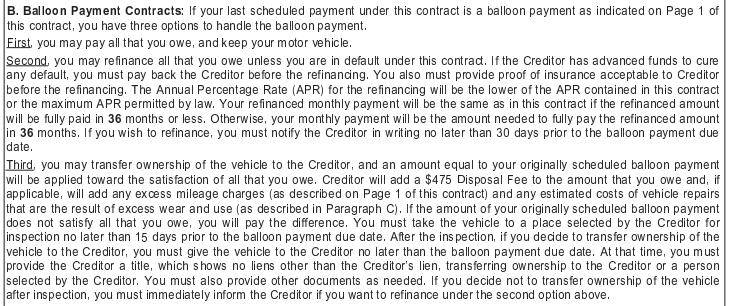

Here is an example of what my contract says (see the "Second" option):

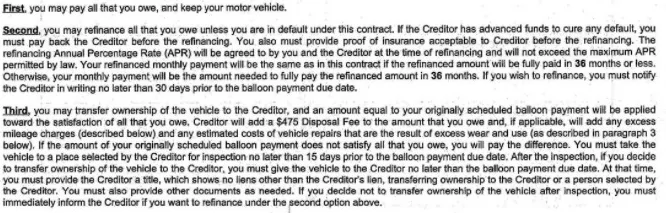

Here is another example with slightly different language.

Sponsored

Last edited: