generaltso

Well-Known Member

- Joined

- Jun 24, 2020

- Threads

- 76

- Messages

- 15,389

- Reaction score

- 28,696

- Location

- Vermont

- Vehicles

- 2024 Kia EV9 GT-Line

That‘s not Ford Options.I was fortunate back in August 23. 0% for 60 months.

Sponsored

That‘s not Ford Options.I was fortunate back in August 23. 0% for 60 months.

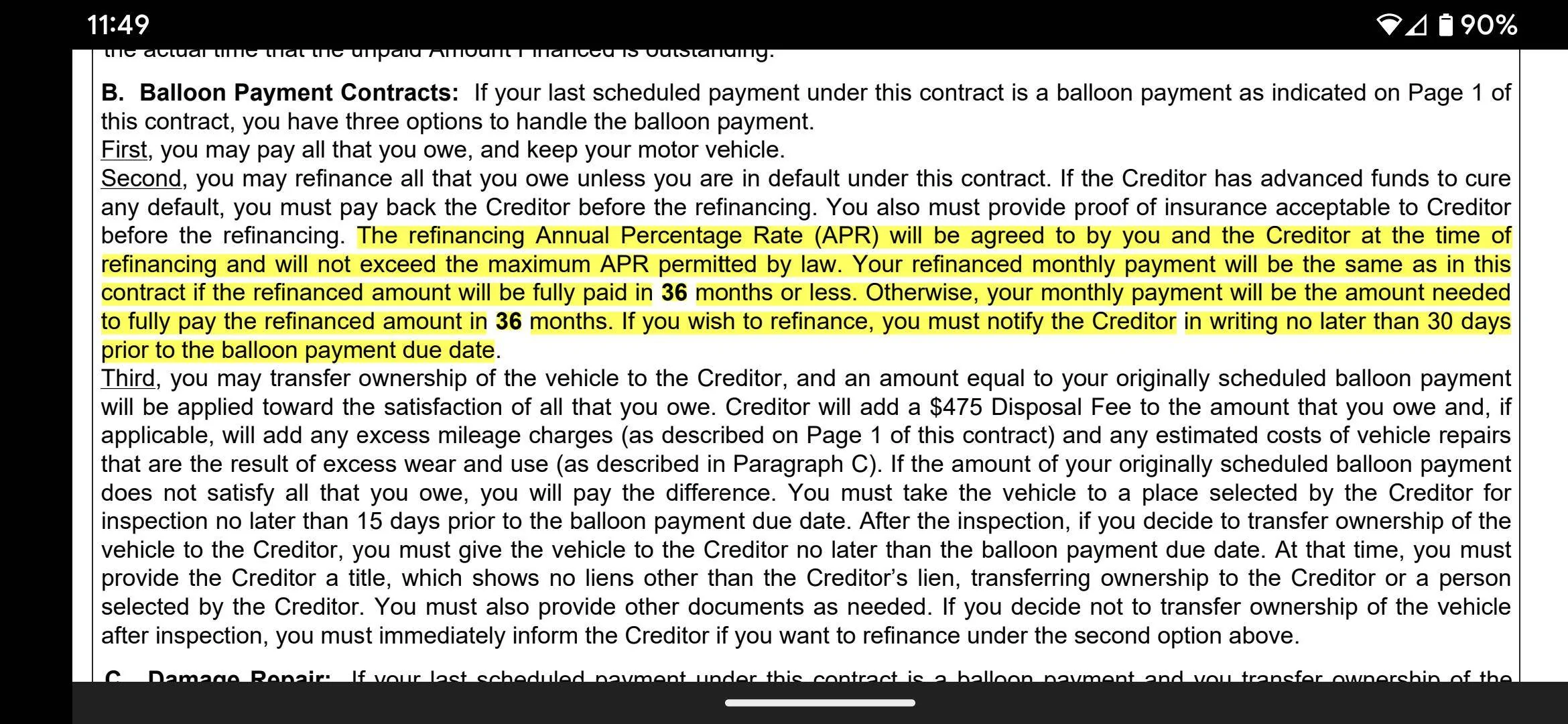

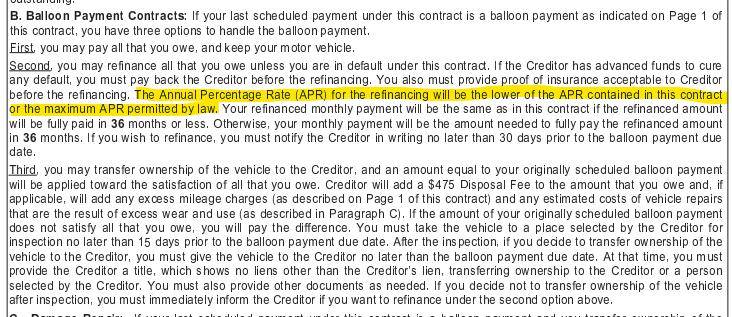

That language differs from my contract, which says the APR will be the lower of the APR agreed to and the APR permitted by law. But the refinanced payment will increase to 10% higher than the current payment.Sure, and for many regions, it was pre-determined in the contract terms. The terms on my loan aren't as clear, so I needed to call to find out how it'll work.

I hesitated to post the info today because it's not a done deal until at least another month from now. Nothing is in writing yet. (At least, per my own loan contract here in Arizona.)

That sounds more like a FlexBuy contract than Ford Options.That language differs from my contract, which says the APR will be the lower of the APR agreed to and the APR permitted by law. But the refinanced payment will increase to 10% higher than the current payment.

Personally, I'm not ready to let my Mach-e go, but could be next year. I'd prefer to keep it until the new shiny comes out.

Please inform how you make out. 2.25% rate for me would be fantastic.That's what I'd assumed until I called and spoke with Ford Credit. As I said, I'm holding out hope but there's no guarantee until I work through the details with them next month.

That language differs from my contract, which says the APR will be the lower of the APR agreed to and the APR permitted by law. But the refinanced payment will increase to 10% higher than the current payment.

it is a Ford Options contract. I am referring to the balloon payment term.That sounds more like a FlexBuy contract than Ford Options.

FlexBuy is 66 or 75 months split into two different payment schedules (no balloon payment). Ford Options on the other hand was 36 or 48 months. Which was either 35 or 47 monthly payments and 1 balloon payment.

Ah, OK. It was the "But the refinanced payment will increase to 10% higher than the current payment." part that was confusing. I've not seen that in the contract text before.it is a Ford Options contract. I am referring to the balloon payment term.

Is that the guaranteed rate or are they honoring everyone’s existing rate? If I can get my .9% or 1.9% (can’t remember which) GT’s qualified for, that would be amazing.Yeah, next year when my Options contract is up I'll refi for 2.25%. Don't need to do anything with the dealer. Just call Ford Credit immediately after your final monthly payment has posted (last monthly payment before the balloon is due).

Yes, that's more or less right. Put a little more concise: Ford Options is a simple interest loan with just one twist: the final month's payment is enormous.Is that the guaranteed rate or are they honoring everyone’s existing rate? If I can get my .9% or 1.9% (can’t remember which) GT’s qualified for, that would be amazing.

Aren’t we kind of paying way more than that in interest though? During this “before the balloon” period, aren’t we paying interest on the full amount? For ease, if the purchase price was $50k and options worked out to $25k principal for the first 3 years, $25k balloon, wasn’t interest applied to the full $50k, than added to the principal and then divided over 36 months? And now we pay interest again on the final $25k?

On my Ford contract, if I refinance the rate will be the lessor of my contract rate or the state maximum rate. So I’ll get the same rate again.Is that the guaranteed rate or are they honoring everyone’s existing rate? If I can get my .9% or 1.9% (can’t remember which) GT’s qualified for, that would be amazing.

Aren’t we kind of paying way more than that in interest though?

The weird thing is hereCurious whether 'rescheduling' the balloon payment with Ford Finance (and maintaining the same loan interest rate) means that this does not require a new loan contract/credit check? If all it entails is just a phone call and less than $1,000 in additional interest over the remaining life of the loan, it does seem like a no brainer not to just keep the car with the same payment. Unless resale values plummet a lot further (I still have over a year left before my balloon).

There's no new credit check.Curious whether 'rescheduling' the balloon payment with Ford Finance (and maintaining the same loan interest rate) means that this does not require a new loan contract/credit check? If all it entails is just a phone call and less than $1,000 in additional interest over the remaining life of the loan, it does seem like a no brainer not to just keep the car with the same payment. Unless resale values plummet a lot further (I still have over a year left before my balloon).