macchiaz-o

Well-Known Member

- First Name

- Jonathan

- Joined

- Nov 25, 2019

- Threads

- 171

- Messages

- 8,579

- Reaction score

- 15,987

- Vehicles

- MY21 J1 Premium RWD SR

The duck is dead.duckduckgo weren't playing nice this morning.

Sponsored

The duck is dead.duckduckgo weren't playing nice this morning.

I would ask for a representative (an officer of the corporation, or another agent designated to represent the company) of the dealer to either put it in writing that you must buy the extended warranty in order to get the publicly offered financing in the car. If they won't put that demand in writing (and they won't) then they should drop it from any further conversation.Hello there,

Some preface... What I'm trying to make sure here is that I don't get f***ked by the dealership/finance guys out of money. So I'm asking for advice on how I should handle this situation moving forward. Please help me get out of this mess...

At time of purchase of my Mach-E the guys said that Ford Options was not an option in California (wrong). I said lets go ahead with regular financing because I wanted to take the car home with me that day. After speaking with their GM about Ford Options, he said that they will re-do my contract. Effectively cancelling the current contract and starting a new one with Ford Options. I will be the first one at their dealership to get Ford Options. After briefly meeting with the finance guy today to look at some preliminary numbers, to my surprise the Ford Options monthly payment total came out to be exactly the same as my regular financing - ~$1,050/mo. Something smells fishy here...

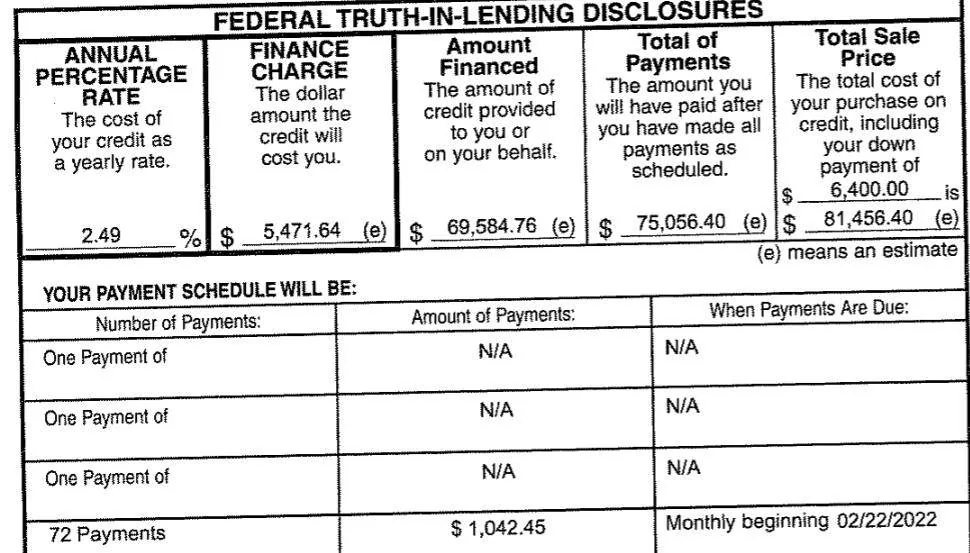

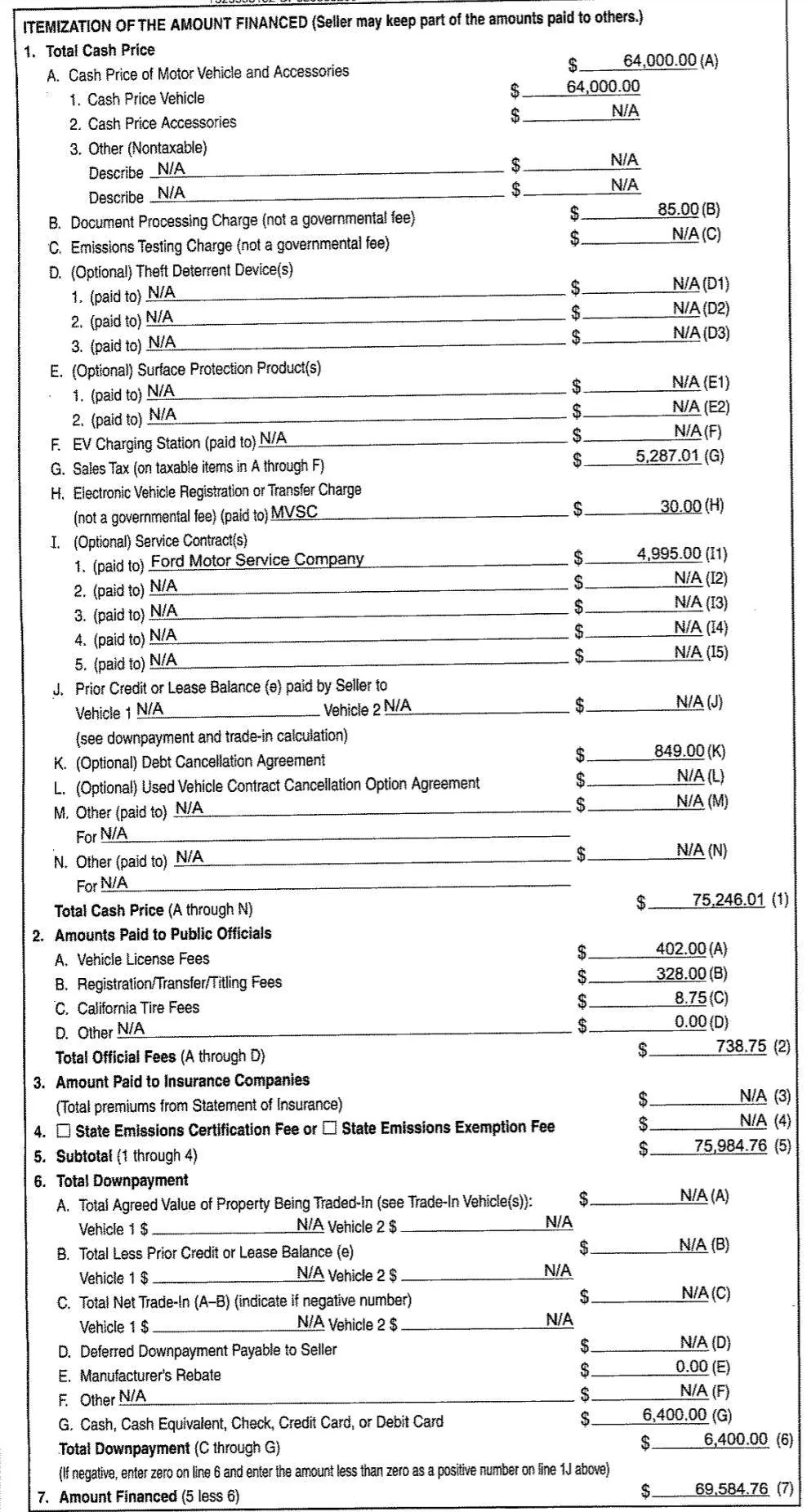

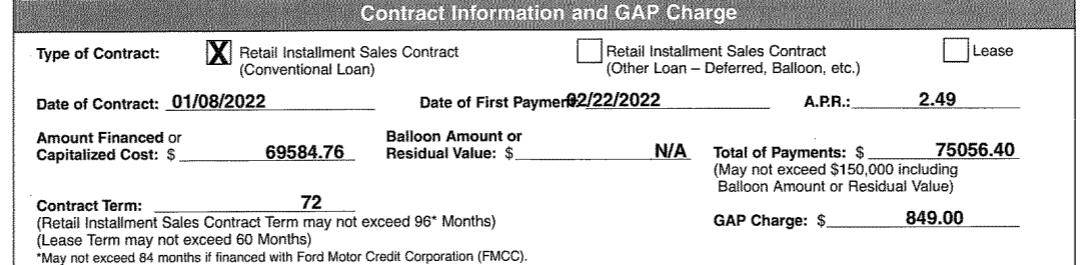

Car sale price - $64,000 (includes $8,000 ADM)

Regular finance purchase -72 months, 2.49%, $6,400 down.

Ford Options Plan - 48 months, 2.49%, 10,500 miles/yr, $6,400 down.

Credit score -~770.

Upon checking and comparing to the estimating payment on the Ford Build-a-Mach-E website I saw some MAJOR differences. Their estimate was that I should be paying roughly $680/mo with a sale price of $64,000 and $6,400 down (website did give me a estimated APR of 1.4%, but shouldn't be that big of a difference).

Now that I look back on the day of purchase there was a major red flag that I looked past. The finance guy said that I will only be able to get the 2.49% if I get the extended warranty and GAP protection. My original APR was like 3.49%. This would only raise my monthly bill by $10. "No brainer, right?" (His words). I said sure, let's add the extended warranty and GAP protection... There was also some fees involved during the process that I looked past (I will post my original contract details below).

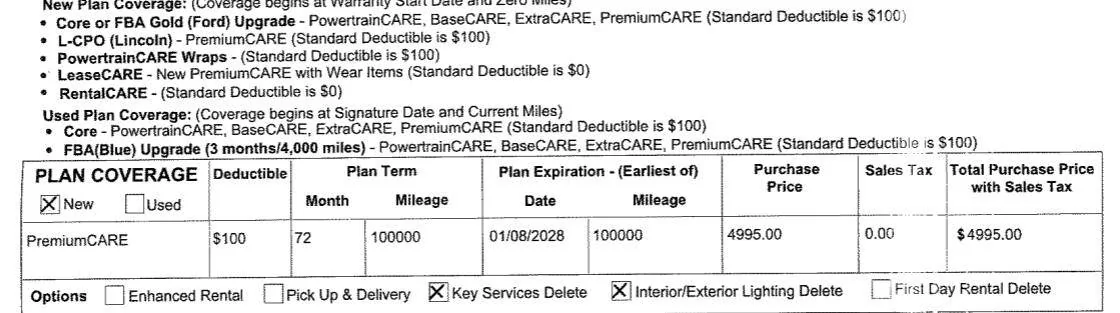

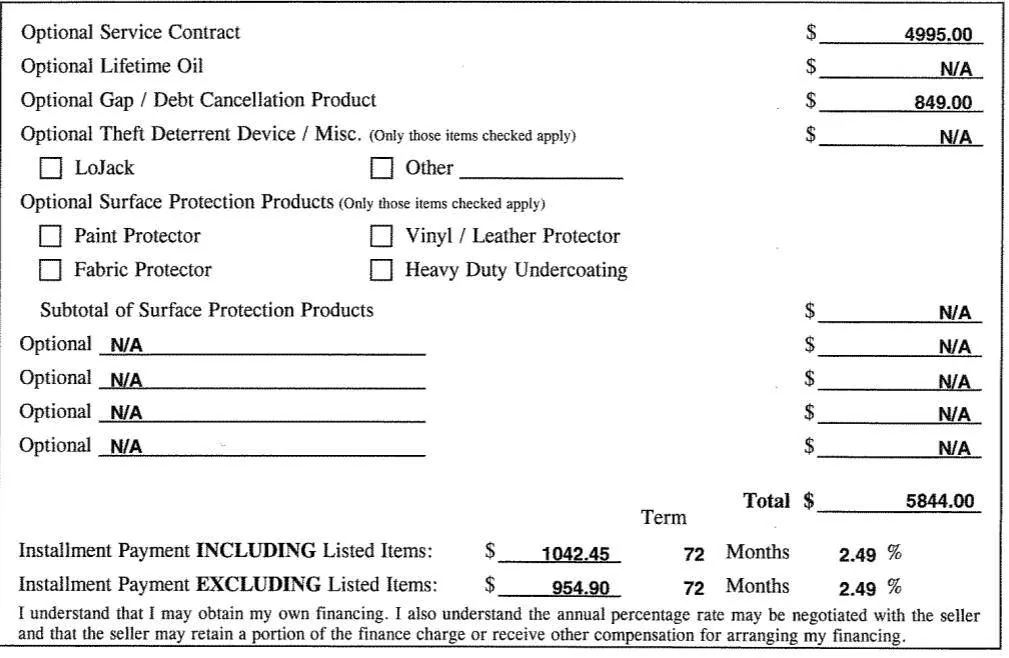

What I think is happening now is that they are trying to get me to pay the same fees and buy the extended warranty + GAP protection with the Ford Options plan. Hence the big price difference... Since they are cancelling my original contract, can I avoid purchasing the extended warranty, gap, and argue for them to not include these absurd fees (e.g. $4,995 optional fee to the Ford Motor Service Company, I guess this is the extended warranty)?

Here's my original contract details (in process of getting nullified/cancelled in favor of a Ford Options contract):

EXTENDED WARRANTY

GAP:

VEHICLE CLOSING STATEMENT:

In summary:

1. Can I reject the extended warranty and GAP protection from my original contract agreement which will be nullified prior to starting the Ford Options agreement? Dealership is trying to keep these...

2. Is it true that to get a lower APR I have to get extended warranty?

3. What APR should I be expected to pay with a ~770 credit score and 10% down?

4. I'll take any advice you can give me.

They wouldn't sell warranties if the payout was more than the price of the warranty. Sure, some people will get their money back, or more, but there are better bets.I have to disagree about the extended warranties. They are are good thing to have if you plan on keeping your car past the 3/36 warranty. They have saved a lot of people from major expenses. I do agree with you though about the $5k price. That's waaaay overpriced.

Why is $400 a magic number vs $800?GAP is definitely not a waste of money if you can get it for $400, even if you're confident in your own ability, you never know other drivers. With today's market, I would NOT get GAP unless you're paying an ADM. GAP is also pointless with a hefty downpayment, which it seems like you put down.

So what if there is an $8K difference? What are the odds he'll wreck it to the point that it isn't fully repaired and he has to eat part of it? Then take those odds, do some math, and see what the expected return is on the $800. I'll just about guarantee you the $800 is too much, but it's probably claser to $0.00 than $800 for a fair gap price.I'm CLEARLY stating that he should buy GAP because he has an ADM but you're saying don't get GAP because that means you can't afford the car. What

It's worse than that because that $8,000 will lead to another $1,000 in TTL in California.You are paying around $5,500 in interest along with paying $8,000 in ADM charges.

You are essentially paying $13,500 in "extra" fees. And that is w/o the GAP and Extended Coverage?

I would definitely take the car back if you can.

This is crazy money to throw away.

The duck is also grumpy today.The duck is dead.

I would try everything in my power to get out of this purchase. This is a scary one.It's worse than that because that $8,000 will lead to another $1,000 in TTL in California.

Because $400 is around the dealer cost for GAP. If you pay $800+ for GAP then you're paying around 100+% markup.Why is $400 a magic number vs $800?

Nope. The only one who can warranty a car is the manufacturer. Let me clear up your confusion. Here’s a quote from an article by the Federal Trade Commission on their website:You are confusing the Service Plan with a maintenance plan. The Premium Care plan he has a contract for is extending the factory warranty to 6 years 100,000 miles with a $100 deductible.

At $5000 it is not worth it, but at $1500 it may be for OP. I've had it on several of my Ford's and its paid for itself every single time.

The service plan is a Ford plan. Its only honored at ford dealerships. It doesn't cover 100% of what the bumper to bumper warranty covers, but it is almost everything. Yes it does cost money, but its extending the coverage period of the warranty. It works just like the warranty does. Drop it off with the dealer, they bill ford for any repairs. It even includes rental car coverage as standard, which the factory warranty doesn't cover.Nope. The only one who can warranty a car is the manufacturer. Let me clear up your confusion. Here’s a quote from an article by the Federal Trade Commission on their website:

January 15, 2015

by

Colleen Tressler

Consumer Education Specialist, FTC

“Ever wonder about the difference between a warranty and a service contract? Well, wonder no more.

Many consumer products, including cars, appliances and electronic devices come with a warranty — the manufacturer’s promise to stand behind the product. Warranties are included in the price of the product. If a company offers a warranty, it must be available for you to read before you buy — even when you’re shopping by catalog or online. It’s the law. However, what a warranty covers varies. So, when you’re shopping for things by price or style, consider comparing what the warranty covers, too.

A service contract is sometimes called an “extended warranty,” but service contracts are not warranties. A service contract can help you fix or maintain your product for a specific time — like a warranty. But, unlike a warranty, service contracts cost extra. When you’re shopping, compare specific manufacturers and products. You might find that some service contracts give you the same coverage you get from the warranty that is included in the purchase price. Some service contracts cover only part of the product, and some make it nearly impossible to get repairs when you need them. And, if repairs are cheap, you might not really benefit from the extra cost of a service contract.

Auto service contracts are different. They’re sold by car manufacturers, dealers, and independent companies. Usually, they won’t kick in until the manufacturer’s warranty expires. If you’re thinking about an auto service contract, shop around so you understand exactly what you’re buying and to ensure you are not buying overlapping coverage. What you get varies widely, as does what you pay for it, so be sure you know what the service contract covers.

No matter what you’re buying, some consumer advocates suggest that you might be better off skipping service contracts. Instead, they recommend putting that money in a savings account. That way, if you need repairs, you’ll have savings to fall back on. And if you don’t need repairs, you’ll have some cash in the bank”

Hope this clears up your confusion.

Exactly!The service plan is a Ford plan. Its only honored at ford dealerships. It doesn't cover 100% of what the bumper to bumper warranty covers, but it is almost everything. Yes it does cost money, but its extending the coverage period of the warranty. It works just like the warranty does. Drop it off with the dealer, they bill ford for any repairs. It even includes rental car coverage as standard, which the factory warranty doesn't cover.

Just because you don't think they are worth the money doesn't mean no one should buy them. It is totally optional. If OP has no plans of keeping the car past 36 months, then it is definitely a waste of money, But if they plan on keeping it any longer, its been a pretty good investment in my experience. Plus, if you sell the car, you can transfer the warranty to the next owner for $75.

I would never buy a vehicle warranty/service plan that was through anyone other than Ford as those are all ripoffs because they will try and get out of paying for anything you try and claim on them. But the Ford plans are actually useful.

Do they have New car replacement instead?Just called Geico, surprisingly they don't offer GAP insurance...

No insurance is a good idea unless the failure is catastrophic for you. If you can afford to cover the loss, then not buying insurance is better in the long run than buying one. When you are buying insurance you are paying for the actual risks plus insurance company profits.Can you provide a scenario where the GAP is a good thing?

You’re correct. The service Plan sold by Ford dealers to cover service and parts after the expiration of the warranty mimics many of the protections of the original warranty, but after the Ford warranty expires, you have no factory warranty.The service plan is a Ford plan. Its only honored at ford dealerships. It doesn't cover 100% of what the bumper to bumper warranty covers, but it is almost everything. Yes it does cost money, but its extending the coverage period of the warranty. It works just like the warranty does. Drop it off with the dealer, they bill ford for any repairs. It even includes rental car coverage as standard, which the factory warranty doesn't cover.

Just because you don't think they are worth the money doesn't mean no one should buy them. It is totally optional. If OP has no plans of keeping the car past 36 months, then it is definitely a waste of money, But if they plan on keeping it any longer, its been a pretty good investment in my experience. Plus, if you sell the car, you can transfer the warranty to the next owner for $75.

I would never buy a vehicle warranty/service plan that was through anyone other than Ford as those are all ripoffs because they will try and get out of paying for anything you try and claim on them. But the Ford plans are actually useful.